- Developing countries face far higher costs of capital for green transition than developed nations.

- The structural imbalance is expected to take centre stage during climate conference – COP30 negotiations, as a barrier to the global green transition.

- Some global credit rating agencies face criticism for employing biased and opaque methods that undervalue developing countries.

If poorer nations pay more than double the interest rates of wealthier countries to fund clean energy, the global green transition risks faltering. Developing countries are expected to demand changes at the climate conference COP30 in Brazil this November, calling out the ‘built-in bias’ in global finance that makes green projects vastly more expensive in the Global South.

The concern related to the cost of capital or borrowing money needed for the green transition was visible in the open consultation events organised recently by the United Nations Framework Convention on Climate Change (UNFCCC). Here, countries were exploring ways to achieve the Baku to Belem roadmap of $1.3 trillion, a term agreed upon in Baku during COP29. Under this term, all parties will work to mobilise $1.3 trillion per year by 2035 from all sources, which will fund climate action in developing countries. This includes loans too, which come with certain costs or interest rates.

Experts say that this cost gap, driven by high borrowing rates, could determine whether the energy transition succeeds globally or leaves some regions behind.

The International Energy Agency (IEA) tracks the average cost of capital for selected countries, including India. For a 100 MW solar PV project, India’s rate is 10.0-11.5%, compared to the 11.0-13.5% in South Africa. While the IEA does not publish comparable figures for developed nations, other sources indicate that the cost of debt is significantly lower, at around 2.8% in Germany and 5.3% in the United States.

The Columbia Center on Sustainable Investment (CCSI), a joint centre of the Law and Climate Schools at Columbia University, published a report in April that highlighted that Emerging Markets and Developing Economies (EMDEs) face a shortage of funds for the green transition, while around $30 trillion in global savings exists every year, but most of it flows to economies already rich in physical and human capital. This leaves a chronic shortfall of financing for countries that are desperately in need of building their infrastructure and human capital.

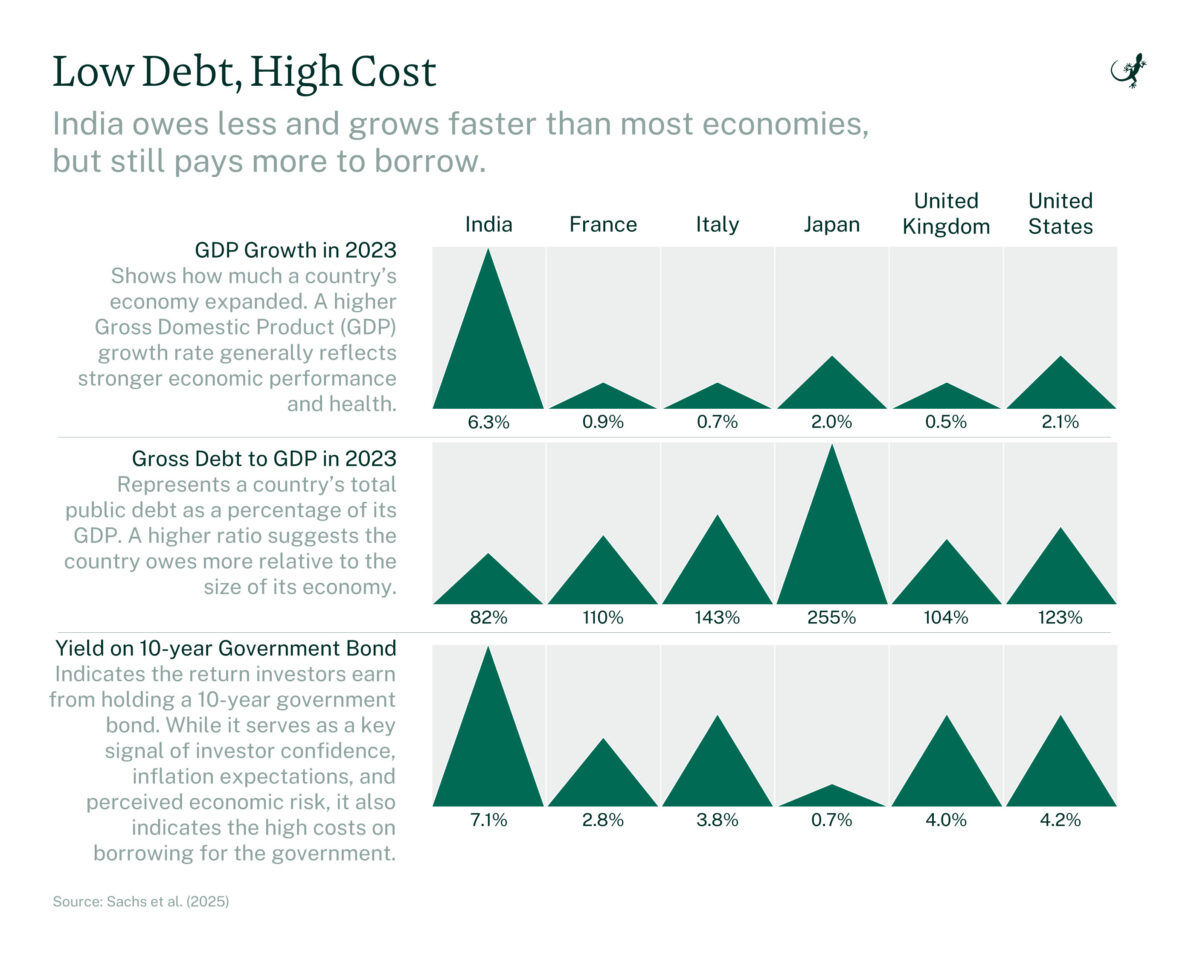

It mentions India as an example and compares it with countries like France, Italy, Japan, the United Kingdom, and the United States. It states that India is performing better in terms of growth rate and debt-to-GDP ratio, which compares a country’s debt to its GDP. Still, India has to pay the highest cost of borrowing among these countries.

The paper connects the higher interest rate with the lower credit rating assigned to countries like India by the credit rating agencies — Moody’s, Fitch, S&P Global. The paper also notes that India’s position still remains stronger due to its large population, which carries a significant weight in credit ratings. The poor ranking by rating agencies not only leads to loss of potential investments and deters investors, but also increases borrowing costs.

Lisa Sachs, the director of CCSI and one of the authors of the paper, says that the cost of capital is “arguably the most critical determinant” of whether climate projects get financed, yet it is rarely addressed in proposals for scaling up climate finance.

Rohit Azad, Assistant Professor at Jawaharlal Nehru University’s Centre for Economic Studies and Planning, calls the current differential in risk assessment “absolutely unfair” and a major barrier for the Global South. “If interest rates are higher, the cost of loans is higher. Green finance is usually costly because setting up new facilities is expensive. Furthermore, high interest rates make these investments even more challenging. It works to the detriment of countries in the Global South,” he says.

Systematic bias

The sovereign rating agencies and their methods have been under scrutiny for a long time due to their methodologies, lack of transparency, and perceived bias. These rankings have a significant impact on countries’ borrowing costs and access to markets, writes Daniel Cash, Reader in Law at Aston University, who adds that the opacity of these ratings can be damaging, especially for African countries.

African countries have also disputed the rating assigned to them. Nigeria and Kenya have registered disagreement over such ratings in recent years, citing a lack of understanding of the domestic environment by the rating agencies.

Similar concerns were raised in the CCSI study. The authors studied the three major credit rating agencies, including Moody’s, Fitch, and S&P Global. They concluded that these agencies systematically assign lower credit ratings to low-income countries (LICs) and lower-middle-income countries (LMICs).

Looking at sovereign ratings by income group, the study found that 125 of the 193 U.N. member states are rated by Moody’s. Of these, 59 are investment-grade and 66 are below investment-grade. Among high-income countries, nearly three-quarters have investment-grade ratings. This drops to less than one in five for upper-middle-income countries, about one in 25 for lower-middle-income countries, and none for low-income countries. In total, only 12 of the 130 developing countries hold an investment-grade rating, according to the analysis conducted by the CCSI authors.

The paper also notes that per capita GDP is a direct determinant of sovereign credit scores, with higher GDP per capita translating into higher ratings. Population size is another factor given positive weight, which helps explain why India and the Philippines, both populous LMICs, hold investment-grade ratings while other LMICs do not. The debt-to-GDP ratio doesn’t seem to matter much for credit ratings, as many wealthy countries still receive the highest ratings, even though they owe more than their entire yearly economic output.

Sachs says, “There are two foundational problems with existing sovereign credit ratings. One is the inherent biases and structural flaws in the methodologies used by the three dominant credit rating agencies. The other, perhaps even more fundamental flaw, is the idea that a country’s ability and likelihood to repay a loan can be reduced to a single score, irrespective of the nature of the loan or the country’s structural conditions and reforms.”

“That single score lumps together completely different kinds of risk, ignores whether the debt is short-term or long-term, for consumption or for investment, and overlooks the fact that productive public investment can strengthen a country’s creditworthiness over time,” she continues.

The realisation is not new. Misheck Mutize, Lead Expert on Credit Rating Agencies for Africa at the African Union and a lecturer at the University of Cape Town, shares that African countries have repeatedly raised the issue that ratings “do not always reflect their actual risk profiles and economic fundamentals, often leading to higher borrowing costs.”

Azad argues that the current system is “totally biased,” pointing to the way Global South nations are treated as unstable, while countries like the United States, where political and policy uncertainty is also high these days, escape such scrutiny. “If risk is the key factor, then the riskiest country might be the U.S. because of policy uncertainties and total lack of transparency under leadership of Donald Trump,” he notes.

There has been a long-standing demand to reform the approaches and methodologies of the ‘Big Three’ global rating agencies.

Impact of high cost

Emerging markets and developing economies (EMDEs) outside China continue to face disproportionately high costs of capital for clean energy projects, driven by both real and perceived market risks, according to a recent U.N. report. This financing gap is reflected in the growth of renewable energy: of the 4,448 GW of global renewable capacity installed by the end of 2024, 41% was in China, 39% in OECD countries, and nearly half of the remaining 20% in Brazil and India. Africa accounted for just 1.5%.

The impact of high interest is huge. According to the IEA, a one percentage point reduction in the cost of capital could lower financing costs for EMDE net-zero transitions by $150 billion per year. There are several studies that highlight that even small differences in interest rates have huge impacts on energy costs in the Indian context. One study says that a one-percentage-point increase in the cost of capital can raise electricity costs by about 5%, while another says that a 2% rise (for example, from 10% to 12%) or fall in interest rate can change solar tariffs by roughly 7%.

Sachs says, “The cost of capital is one of the most decisive factors in determining whether renewable energy and other climate investments happen at the speed and scale required. From an EMDE perspective, high costs of capital delay, shrink, and sometimes entirely prevent critical infrastructure investments. These investments are not only essential for climate action but also for achieving universal access to reliable and affordable energy, expanding sustainable transport, and building resilient and inclusive cities.”

The CCSI paper mentions India as an example, having good indicators but still facing high borrowing costs. But India has seen a manifold growth in renewables. Solar capacity has grown from 2.82 GW in 2014 to 110.9 GW in 2025.

When asked how she sees India’s achievement in renewables and the high cost of capital together, Sachs appreciates India’s story and says, “But it’s also a story of how much more could be done if the cost of capital were lower. Many successes have relied on strong policy frameworks, innovative domestic financing, multilateral support, and the ability to attract foreign capital despite risk premiums. Yet even here, high costs mean higher tariffs, slower uptake in some regions, and difficulty financing riskier technologies like storage or green hydrogen. If India could access capital on terms closer to advanced economies, we could see much faster deployment, deeper decarbonisation, and more inclusive access to clean energy.”

Mongabay India reached out to all three credit rating agencies to understand their methodologies and received no response at the time of publishing.

Read more: Just transition policy should focus on social infrastructure, apart from alternative jobs: report

Banner image: Workers install solar panels in Gujarat. (AP Photo/Rafiq Maqbool)